Long before the phrase “death tax” entered political vocabulary, Americans were already debating the idea of an estate tax: Should the government tax wealth as it passes from one generation to the next?

The death tax history in the United States is not just a story about revenue. It’s a story about war, inequality, and shifting ideas about fairness that stretches back more than two centuries.

Table of Contents:

What Is the “Death Tax”?

Despite the ominous name, the “death tax” is not an official term.

It refers to the federal estate tax, which is levied on large estates before assets are passed on to heirs. Today, only estates above a high threshold, typically in the millions, are subject to the tax, meaning most Americans will never encounter it directly.

Still, like death and taxes, the phrase “death tax” has endured, shaping public perception far more than the technical policy itself.

Early Roots: Death Taxes Born in Crisis

The origins of the death tax in America are closely tied to moments of national urgency and death, ironically.

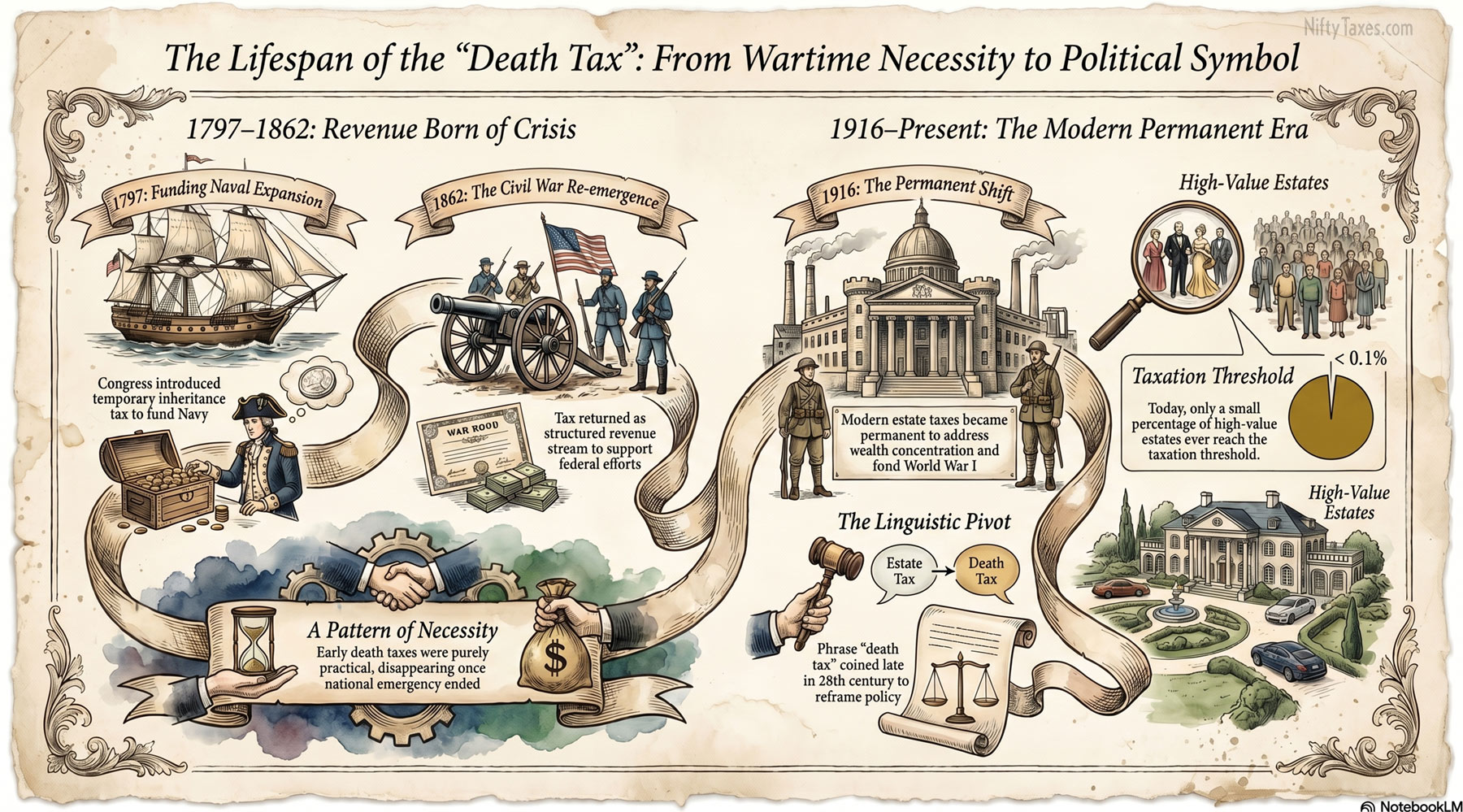

In 1797, amid rising tensions with France, Congress introduced a temporary tax on inheritances to help fund naval expansion. This estate tax was a practical solution to an immediate problem, and once the crisis passed, the tax quietly disappeared.

This pattern would repeat itself.

During the American Civil War, the federal government once again turned to inheritance taxes to generate revenue. Established in 1862, this version was more structured, reflecting a growing federal role in taxation. Yet like its predecessor, it was repealed after the war ended.

In these early chapters of death tax history, the policy was less about ideology and more about necessity.

1916: A Turning Point

The modern estate tax emerged in 1916, against the backdrop of global conflict and domestic change.

As World War I loomed, Congress enacted a permanent federal estate tax; not only to raise funds, but also to address concerns about concentrated wealth. The United States was entering a new era of industry, one in which vast fortunes could be accumulated, and passed down intact.

Supporters argued that taxing large estates could help maintain economic balance. Critics, however, saw it as a form of double taxation, penalizing families for transferring assets that had already been taxed during a lifetime.

The debate, once rooted in wartime necessity, had become philosophical.

Why Death? The Rise of a Loaded Term

For decades, the estate tax policy remained relatively technical, debated mostly among lawmakers and economists.

That changed in the late 20th century, when the phrase “death tax” gained traction.

It was a linguistic shift with real consequences. By framing the estate tax as a tax on death itself, opponents recast the issue in more emotional terms. What had once been a question of fiscal policy became a matter of principle.

I mean, what politician wants to defend their support for the “death tax” in a debate?

Even today, the terminology shapes how the tax is understood, and misunderstood.

The Death Tax Today

Modern estate tax policy bears little resemblance to its early forms. Today:

- Only a small percentage of estates are taxable

- The threshold for taxation is set at a high level

- Some states impose their own estate or inheritance taxes

In practical terms, the tax applies primarily to the wealthiest households. Yet its symbolic importance remains far greater than its reach.

At what level are estates taxed? Trump’s Big Beautiful Bill permanently sets the federal estate tax exemption at $15,000,000 per individual and $30,000,000 per married couple

A Few Lesser-Known Facts

The history of the death tax contains its share of surprises:

- The death tax, or “federal estate tax” has been repealed and reinstated multiple times

- In 2010, it temporarily vanished for a single year

- Early inheritance taxes sometimes varied based on how closely related the heir was to the deceased

These details reveal a system that has never been static, but constantly reshaped by circumstance and debate.

Why the Death Tax Still Sparks Debate

The persistence of the estate tax is not simply a matter of economics.

It reflects a deeper question: What role should taxation play in shaping opportunity across generations?

For some, the estate tax represents a modest check on inherited wealth. For others, it is an unnecessary intrusion at a deeply personal moment.

The long arc of death tax history suggests that this tension is unlikely to disappear. Like many aspects of the American tax system, it continues to evolve, shaped as much by values as by numbers.

Death Tax FAQs

The death tax is another name for the estate tax, which applies to large estates when someone dies. It is paid before assets are passed to heirs.

The first version appeared in 1797, but the modern estate tax was established in 1916. In 2025, Trump’s Big Beautiful Bill permanently raised the exemption to $15 million per person.

No. The death tax (estate tax) is paid from the estate before assets are distributed, while an inheritance tax is paid by the person who receives the assets. The federal government has an estate tax, but only some states impose an inheritance tax.

No. Only a small percentage of high-value estates are subject to the federal estate tax in America today.