If you’ve ever wondered why tax rates feel like they’re constantly shifting, the answer is simple: they are. The story of tax rates by President is less about steady policy and more about reaction to events like wars, economic crises, political philosophy, and changing ideas about fairness.

From the Civil War to modern debates, income tax rates in the United States have swung dramatically depending on who was in office and what the country was facing at the time.

Table of Contents:

When Did Income Taxes Begin?

Before diving into tax rates by President, it helps to understand where it all started.

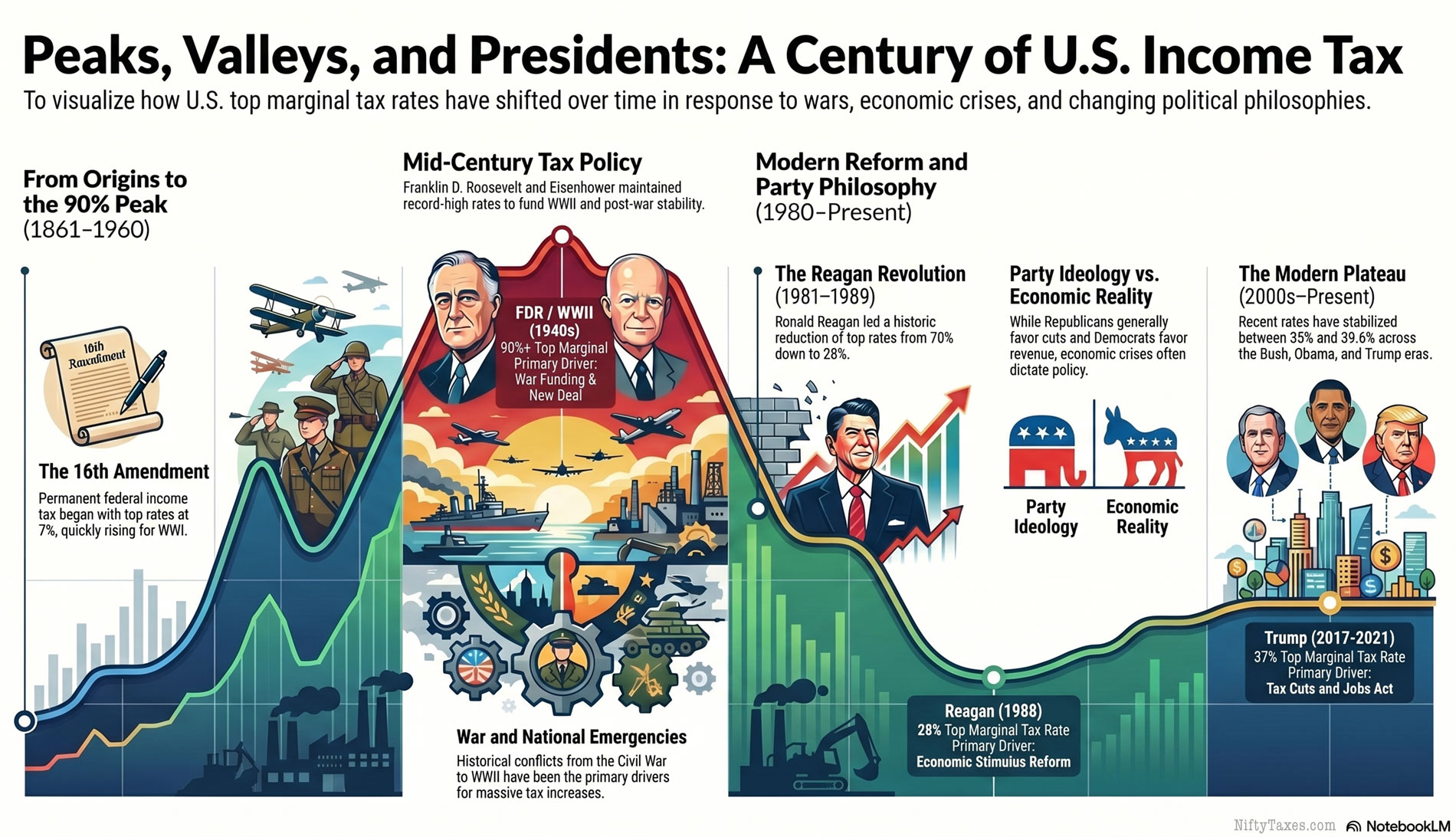

The first federal income tax appeared under Abraham Lincoln in 1861 to fund the Civil War. It was temporary and eventually repealed. The modern income tax system didn’t fully arrive until the 16th Amendment in 1913, which gave Congress the authority to tax income permanently.

From that point forward, presidents and Congress began shaping tax policy in more lasting ways.

Key Tax Rate Changes by President

Here’s a simplified look at major shifts in top marginal income tax rates under key U.S. Presidents:

- Abraham Lincoln (1860s)

Introduced the first income tax (rates up to ~10%) to fund the Civil War. - Woodrow Wilson (1913–1921)

After the 16th Amendment, top rates started at 7% but quickly rose to over 70% during World War I. - Calvin Coolidge (1923–1929)

Oversaw major tax cuts, lowering top rates to around 25% during the Roaring Twenties, a period of economic growth. - Herbert Hoover (1929–1933)

Taxes raised in 1932 during the Great Depression. Not helpful! - Franklin D. Roosevelt (1930s–1940s)

Raised top rates dramatically, eventually above 90%, to fund New Deal programs and World War II. - Harry Truman (1945–1953)

Maintained high wartime rates. - Dwight D. Eisenhower (1953–1961)

Maintained very high top rates (around 90%) during a period of post-war stability. - John F. Kennedy / Lyndon B. Johnson (1960s)

Cut top rates from over 90% to around 70% to stimulate economic growth. - Ronald Reagan (1981–1989)

Led sweeping tax reform. The Tax Reform Act of 1986 lowered top rates from 70% to 28%, one of the largest reductions in history. - Bill Clinton (1993–2001)

Increased top rates modestly to around 39.6% as part of deficit reduction efforts. - George W. Bush (2001–2009)

Reduced top rates again to 35%, emphasizing tax relief and economic stimulus. - Barack Obama (2009–2017)

Raised top rates back to 39.6% for higher-income earners after the financial crisis. - Donald Trump (2017–2021, 2025-2028)

Lowered the top rate slightly to 37% through the Tax Cuts and Jobs Act of 2017.

Why Presidents Raise or Lower Tax Rates

Looking at tax rates by President, a clear pattern emerges: tax policy follows circumstances.

1. War and National Emergencies

Wars have historically driven tax increases. From Lincoln to Roosevelt, major conflicts required massive government spending, often funded through higher taxes.

2. Economic Crises

During downturns, presidents often adjust tax rates to stabilize the economy by either raising revenue or encouraging spending.

3. Political Philosophy

Income tax rates also reflect broader beliefs:

- Some leaders favor higher taxes on top earners to fund government programs

- Others prioritize lower taxes to encourage investment and growth

4. Deficit and Budget Pressures

When deficits grow, tax increases often return to the conversation, regardless of a President’s political party.

Interesting Patterns in Tax Rates by President

A few surprising trends stand out:

- The highest tax rates in U.S. history (over 90%) occurred in the 1940s and 1950s

- Tax cuts and increases often happen in cycles rather than straight lines

- Even large changes rarely happen overnight, and are usually phased in over time

Perhaps most interesting is how tax policy reflects the priorities of each era more than any single president’s agenda.

Tax Rates: Republican vs Democratic Presidents

At a high level, there is a general pattern in income tax rates by President: Democratic presidents have more often supported raising or maintaining higher top income tax rates, while Republican presidents have typically pushed for lowering them.

This reflects broader political philosophies. Democrats often emphasize using tax revenue to fund social programs, while Republicans tend to prioritize lower taxes to encourage economic growth and investment.

That said, the historical record is not perfectly consistent. Context matters. For example, Franklin D. Roosevelt, a Democrat, raised rates dramatically during the Great Depression and World War II, but those increases were driven as much by necessity as ideology.

On the other hand, Republican presidents like Ronald Reagan pursued major tax cuts in the 1980s, while also supporting reforms that broadened the tax base. Meanwhile, some Democratic presidents, such as John F. Kennedy, implemented significant tax cuts to stimulate the economy.

In practice, tax policy tends to follow economic conditions more than party lines alone. Wars, recessions, and budget deficits often play a larger role than political affiliation. While party trends can offer a rough guide, the history of income tax rates shows that both Republican and Democratic presidents have raised and lowered taxes when circumstances demanded it.

Why Tax Rate History Still Matters

Understanding tax rates by President helps explain today’s debates.

Modern tax discussions, whether about fairness, growth, or government spending, are part of a much longer story. The numbers may change, but the underlying questions remain the same.

Who should pay more? How much is too much? And what role should taxes play in shaping the economy?

As certain as death and taxes, history doesn’t settle those questions, but it does give them context.

FAQs About Tax Rates by President

The first income tax was introduced in 1861 under Abraham Lincoln, but the modern system began after the 16th Amendment in 1913.

Franklin D. Roosevelt oversaw some of the highest tax rates in U.S. history, with top marginal rates exceeding 90% during World War II.

No. Tax rates have gone up and down depending on wars, economic conditions, and political priorities.

Generally, yes. Democratic presidents more often support higher top income tax rates, while Republicans tend to favor cuts. However, tax rates by President also depend on economic conditions, and both parties have raised or lowered taxes when needed.